{kind=link}

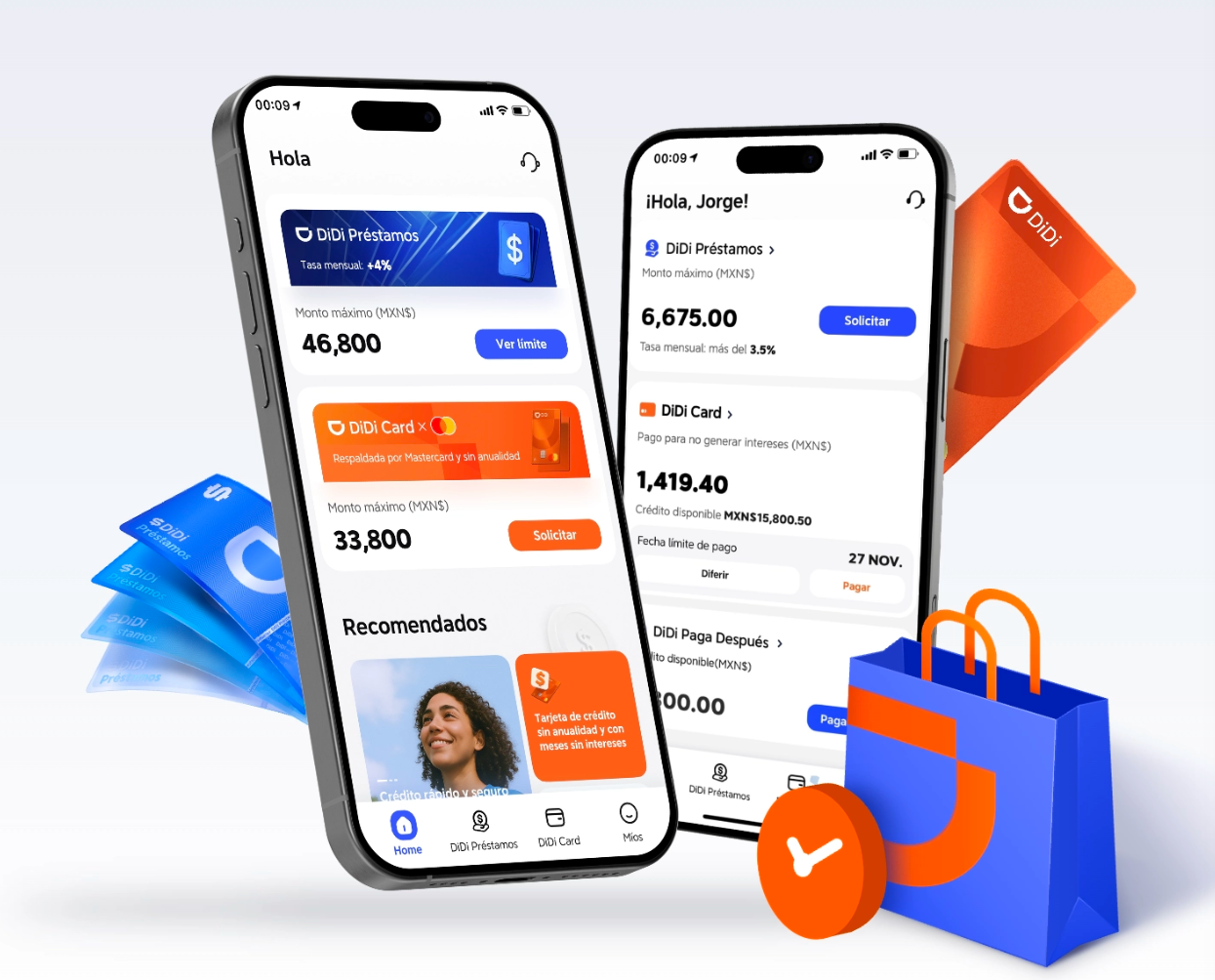

User-first snapshot: what the process feels like

When you hit “apply” for an installment plan, the experience should be simple and clear — and that’s exactly what didi finanzas aims for. This is about you: your timeline, your budget, and whether the payment terms match the compra you want. The platform leans on fintech underwriting and digital KYC so approvals are faster than old-school bank loans, but they still need clean data to move forward.

Core signals that drive approval

Underwriting focuses on a handful of concrete signals that matter most: credit score patterns, recent income stability, payment history, and the requested loan amount versus typical purchase sizes. Those are augmented by device and identity checks — think of them as lightweight fraud prevention. If your credit bureau record shows steady payments and your declared income aligns with the installment plan, the chance of approval climbs quickly.

Documents and digital traces that actually help

Provide recent payslips or invoices, clear ID, and linkable bank activity when possible. The smoother the KYC flow, the fewer manual checks are needed. Also, declare recurring obligations honestly — underwriting looks at debt-to-income implicitly, similar to a loan-to-value mindset for secured products. Clean, consistent statements reduce friction; messy or missing docs trigger manual review and delay.

What commonly slows or blocks approval

Two big culprits trip people up: mismatched identity info, and thin credit history. Mismatched names or addresses force manual verification. Thin credit histories mean the platform leans more on alternative signals like transaction history or employment records. – Small, avoidable mistakes like expired IDs or screenshots instead of PDFs add days to the process.

How DiDi Finanzas fits into Mexico’s regulated fintech scene

Since Mexico’s Fintech Law (2018), platforms operating here have clearer guardrails for consumer protection and data handling. That means faster innovation but also standardized checks across providers in CDMX and other major cities. For users comparing vendors, look for transparent APR disclosures, clear installment breakdowns, and whether a provider reports to credit bureaus — those are practical markers that show a platform behaves responsibly. For reassurance on trust, many searchers ask if didi finanzas es confiable, and the best signal is consistent, documented behavior in complaints channels and reporting practices.

Alternatives and when to choose them

Market alternatives include credit cards, personal loans, and other buy-now-pay-later apps. Choose based on three things: total cost (APR and fees), repayment flexibility (early payoffs, automatic debit options), and approval speed. If you value instant decisions and light paperwork, a fintech installment plan tends to win. If you need a longer tenor or higher credit limits, a traditional loan might be better despite slower processing.

Practical checklist before you apply

Do these five things and you’ll avoid the common friction: make sure IDs match your bank accounts, tidy up recent transactions, confirm monthly income lines, remove small overdrafts if possible, and choose a repayment schedule you can sustain. These prepare the risk assessment and reduce the chance of human review.

Three golden rules to evaluate buy-now-pay-later options

1) Measure true cost: compare APR plus all fees across the full term, not just the monthly amount. 2) Check reporting and dispute pathways: platforms that report to credit bureaus and have clear complaint processes treat your credit responsibly. 3) Match tenor to cash flow: shorter terms reduce interest paid, but don’t overcommit your monthly budget — sustainable payments beat a quick approval every time.

Closing thought and where DiDi fits

These rules help you pick responsibly, and they explain why DiDi’s approach feels practical for many shoppers in Mexico City and beyond — it balances fast decisions with the safeguards modern regulators expect. – Trust builds from predictable behavior, clear terms, and a repayment experience that feels fair. DiDi Finanzas